This just in – MasterCard is set to transform payments tech worldwide.

Well…Woo. Hoo.

You’d think I’d be more excited over this news. But, sadly, I’m not.

While I appreciate the headline, to me, it seems a bit vague and old news. If you’re aligned with the Fintech news and trends, you already heard that everyone, today, is setting to transform payments tech worldwide.

Frankly, I’m tired of hearing that “mobile payments will become more popular in the future,” or “the consumer lifestyle is increasingly defined by the ubiquitous smart phones and tablets and there is an ever-growing appetite for secure mobile payment.”

Hasn’t this already been clear for some time now?

I’m eager to see what MasterCard will really do for consumers and businesses alike, as they claim they are a technology company as opposed to a payments company.

But, in all honesty…enough with the payments technologies. I think I can speak for the rest of the world that we’ve done our fair share of spending and we’re thirsty to adopt behavior change in saving habits.

Hello? Is Anybody Out There?

Is there anybody who can actually help me save already?

Spare me the spiel – I know, I’m an adult and I should be responsible enough to track my spending habits and stir up the motivation and ability to save up each month.

But, I’m also a young woman. I love shopping. And I love dining. Basically, I am a compulsive millennial. (Kuddos to me for the self-awareness.)

I have yet to find a suitable financial application that truly allows me to really focus on helping me foster consistent saving habits.

I’ve done my fair share of research on financial saving apps. It’s quite impressive that these apps are aggregating all my financial data into one screen, providing me suggestions for better saving strategies.

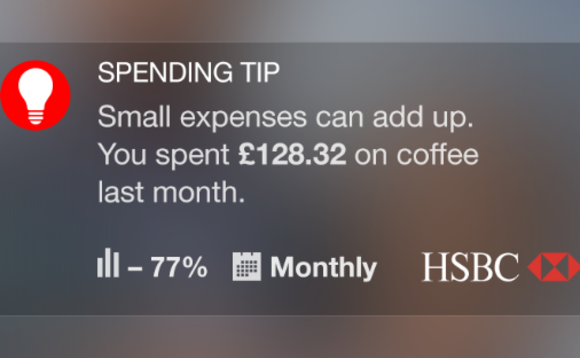

In fact, it has just developed that HSBC has built an app in six weeks that uses real-time analytics and ‘nudge theory’ to alert customers on spending.

For those of you who haven’t heard of the nudge theory, it is a behavioral science concept, which claims that indirect suggestions and positive reinforcement will yield non-force compliance and will influence the decision-making of groups and individuals.

HSBC Nudge was developed by the banks ‘scrum’ collaboration team with hopes that they could move away from the waterfall approach and adopt a more customer-centric approach to building the application.

How the App Works with the Nudge Theory

Targeted nudges are sent to user based on the spending habits analyzed by real-time customer analytics with the aim of informing people of their patterns in expenditure.

According the Danny Palmer, HSBC claims that the use of the nudge theory is “designed to encourage customers to act to support their financial intentions and longer terms goal.”

“We know that many of our customers have good intentions for their financial futures, but that willpower alone is not always enough to drive a long term change in behavior,” states Raman Bhatia, head of digital at HSBC UK.

He further claims, “by incorporating nudge theory into our digital customer communications, we can encourage customers to adjust their behavior to achieve their financial goals.”

Will the Nudge Make Us Budge?

While HSBC is running a trial on the application with the nudge theory, I have hypothetical questions and concerns.

It’s all nice and dandy that I’m getting yet more data on top of my already existing data, but, what the hell am I supposed to do with all of that information?

Bottom line – how can I make sure that at the end of the day, I am on par with my budget and can make saving habits consistently actionable?

Is it enough to provide nudged alerts and suggestions to users today? In all honesty, I’m not so sure – a bold statement, I know.

We need a stronger potion.

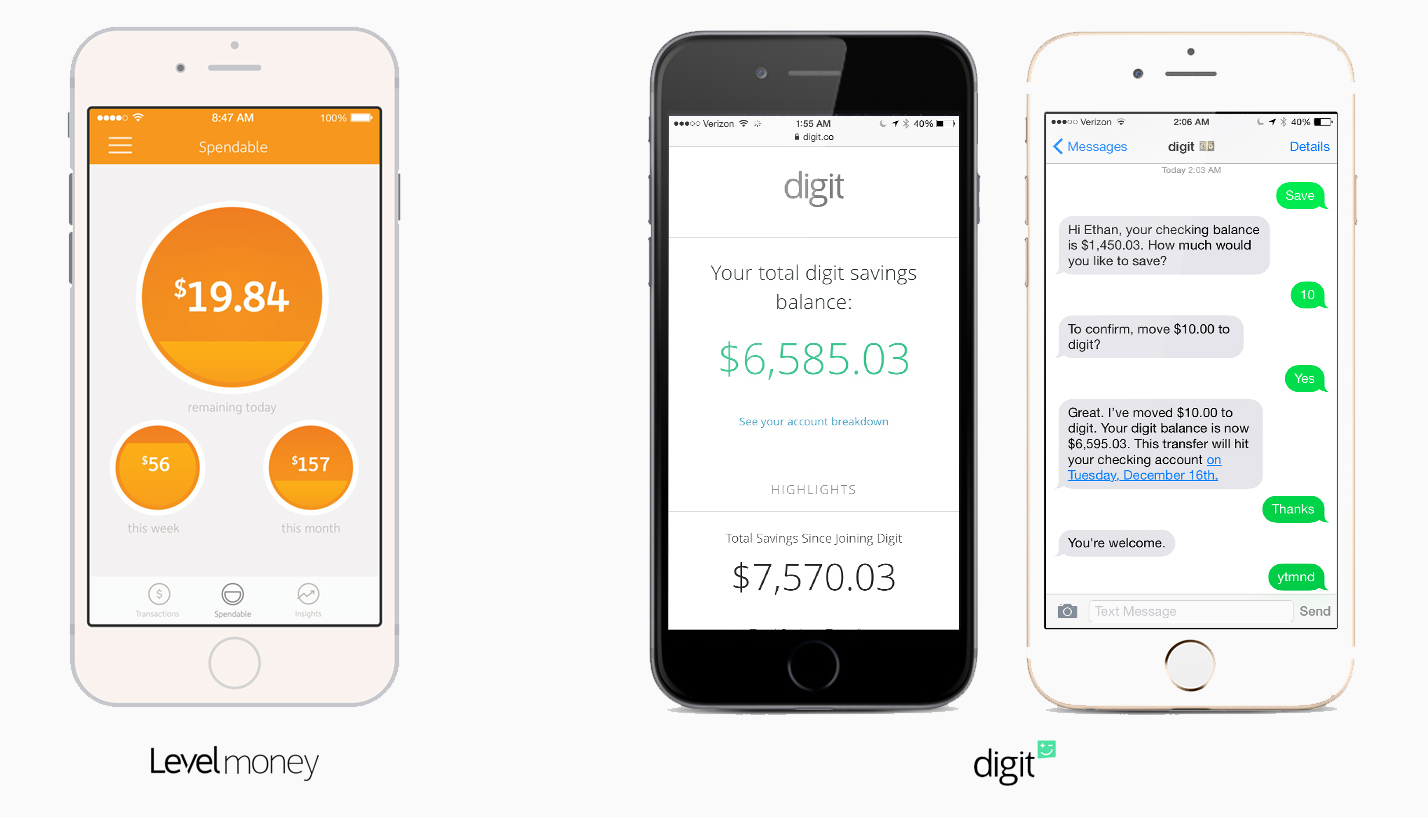

Gaining Control of Daily Finances with Fintech Apps

Frankly, I am impressed with the financial technology startups taking advantage of consumer issues of saving, particularly in the millenial market, automatically emulating budgeting in order to make it easier to save.

Whether or not virtual savings jars, such as Level Money and Digit are the solution? I’m not positively sure. I mean, I have yet to test these applications out.

With the surge in popularity of these apps, I think it’s hard at this point to state if these savings platforms are the key. I can claim that these budgeting and savings apps are attractive and increasingly adopted by consumers. But, where will they stand five years from now?

I do, though, have hopes for HSBC’s trial with the nudge theory and believe that results will show a change in customers behavior; but, whether this theory will prove to disrupt consumer-behavior for financial betterment in this market? I remain skeptic.

Don’t Forget to Follow Us